You’ll find our blog to be a wealth of information, covering everything from local market statistics and home values to community happenings. That’s because we care about the community and want to help you find your place in it. Please reach out if you have any questions at all. We’d love to talk with you!

With all of the unanswered questions caused by COVID-19 and the economic slowdown we’re experiencing across the country today, many are asking if the housing market is in trouble. For those who remember 2008, it’s logical to ask that question.

Many of us experienced financial hardships, lost homes, and were out of work during the Great Recession – the recession that started with a housing and mortgage crisis. Today, we face a very different challenge: an external health crisis that has caused a pause in much of the economy and a major shutdown of many parts of the country.

Let’s look at five things we know about today’s housing market that were different in 2008.

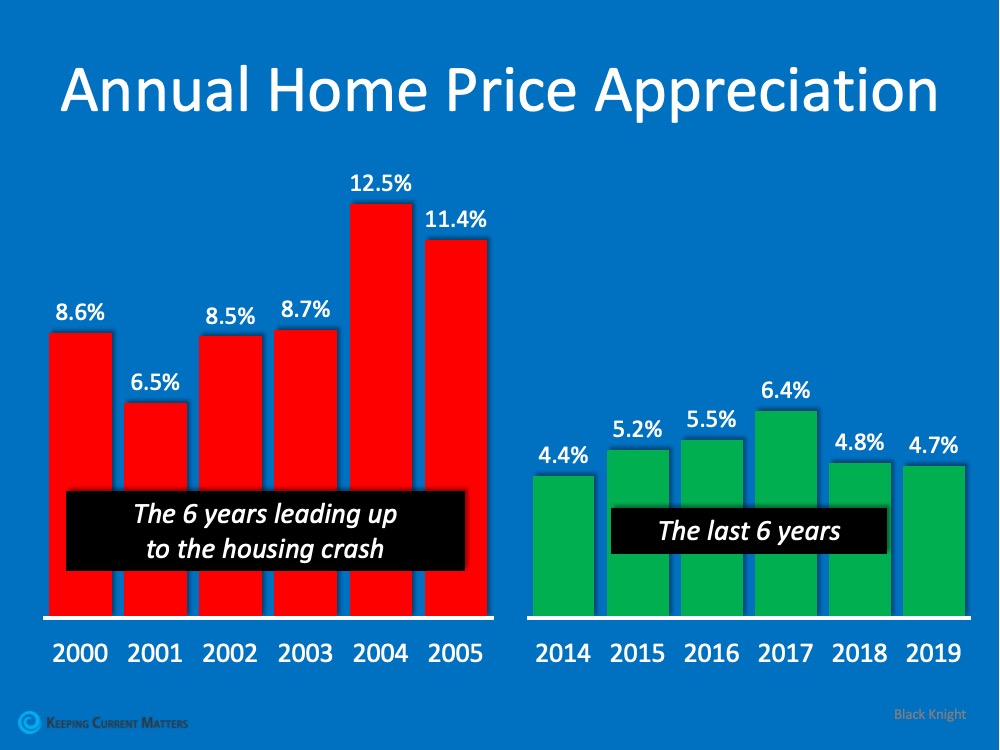

When we look at appreciation in the visual below, there’s a big difference between the 6 years prior to the housing crash and the most recent 6-year period of time. Leading up to the crash, we had much higher appreciation in this country than we see today. In fact, the highest level of appreciation most recently is below the lowest level we saw leading up to the crash. Prices have been rising lately, but not at the rate they were climbing back when we had runaway appreciation.

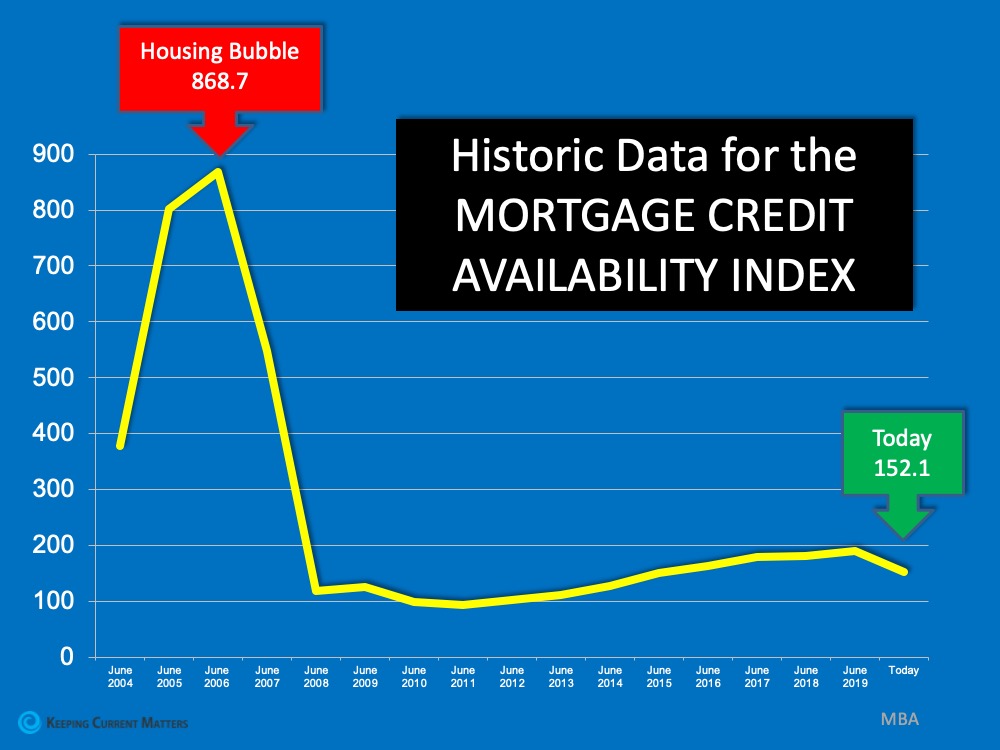

The Mortgage Credit Availability Index is a monthly measure by the Mortgage Bankers Association that gauges the level of difficulty to secure a loan. The higher the index, the easier it is to get a loan; the lower the index, the harder. Today we’re nowhere near the levels seen before the housing crash when it was very easy to get approved for a mortgage. After the crash, however, lending standards tightened and have remained that way leading up to today.

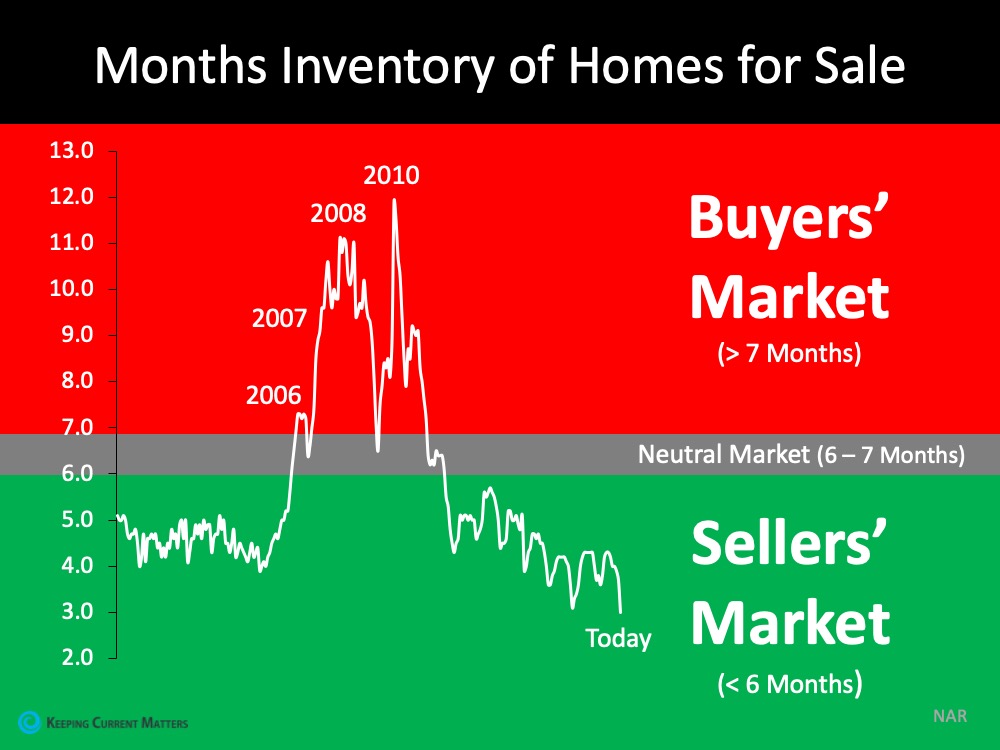

One of the causes of the housing crash in 2008 was an oversupply of homes for sale. Today, as shown in the next image, we see a much different picture. We don’t have enough homes on the market for the number of people who want to buy them. Across the country, we have less than 6 months of inventory, an undersupply of homes available for interested buyers.

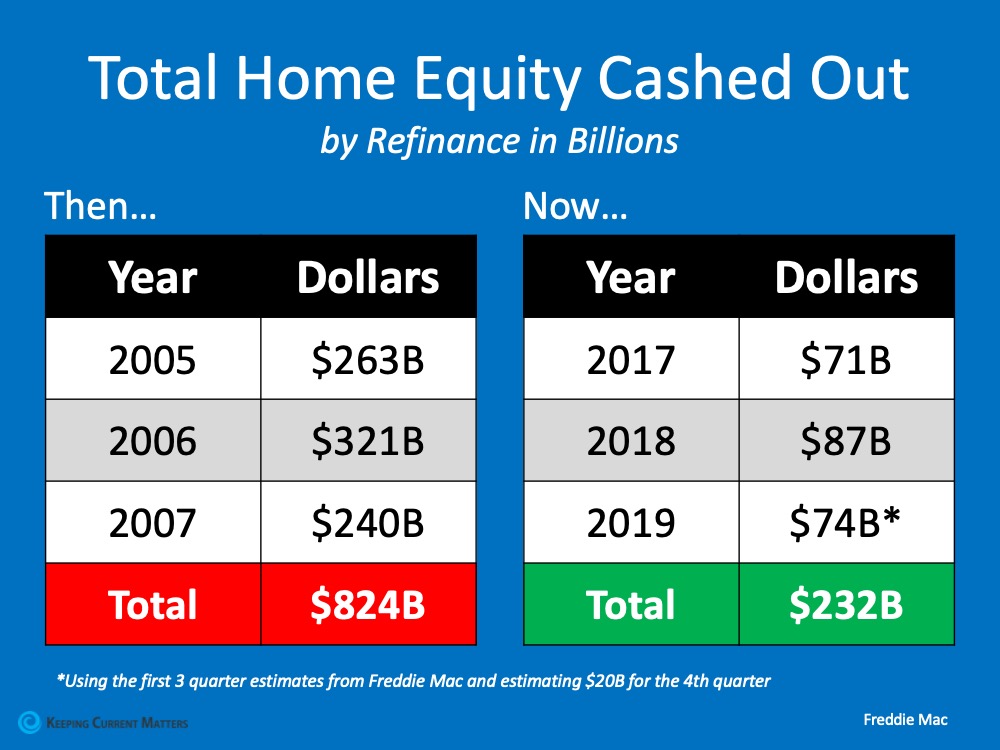

The chart below shows the difference in how people are accessing the equity in their homes today as compared to 2008. In 2008, consumers were harvesting equity from their homes (through cash-out refinances) and using it to finance their lifestyles. Today, consumers are treating the equity in their homes much more cautiously.

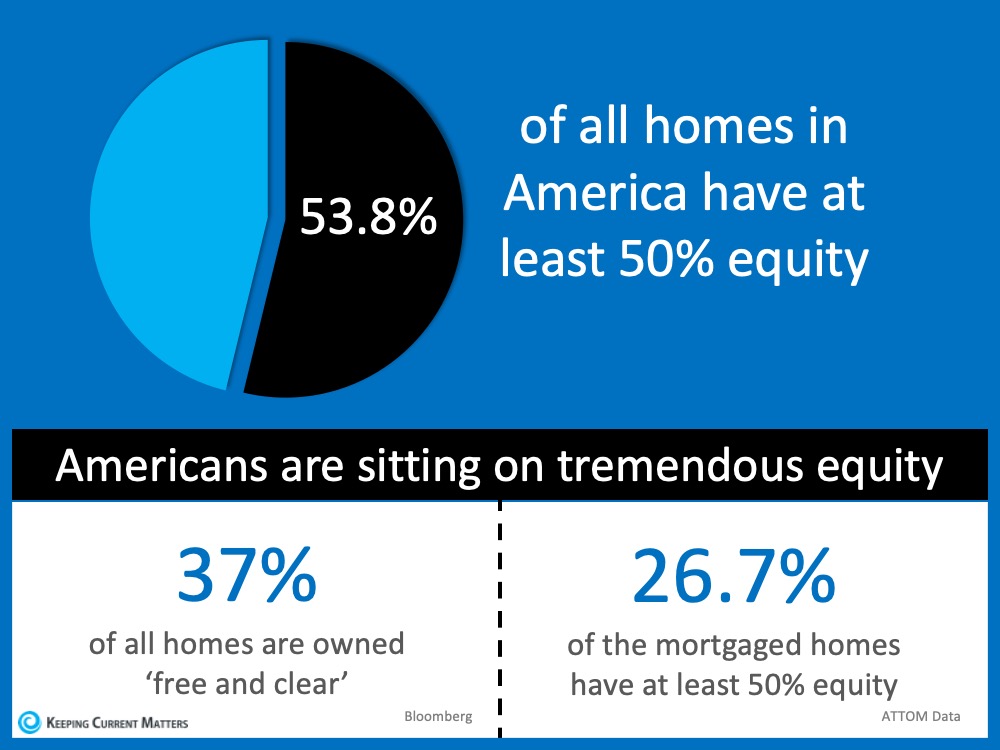

Today, 53.8% of homes across the country have at least 50% equity. In 2008, homeowners walked away when they owed more than what their homes were worth. With the equity homeowners have now, they’re much less likely to walk away from their homes.

The COVID-19 crisis is causing different challenges across the country than the ones we faced in 2008. Back then, we had a housing crisis; today, we face a health crisis. What we know now is that housing is in a much stronger position today than it was in 2008. It is no longer the center of the economic slowdown. Rather, it could be just what helps pull us out of the downturn.

(Source: www.keepingcurrentmatters.com)

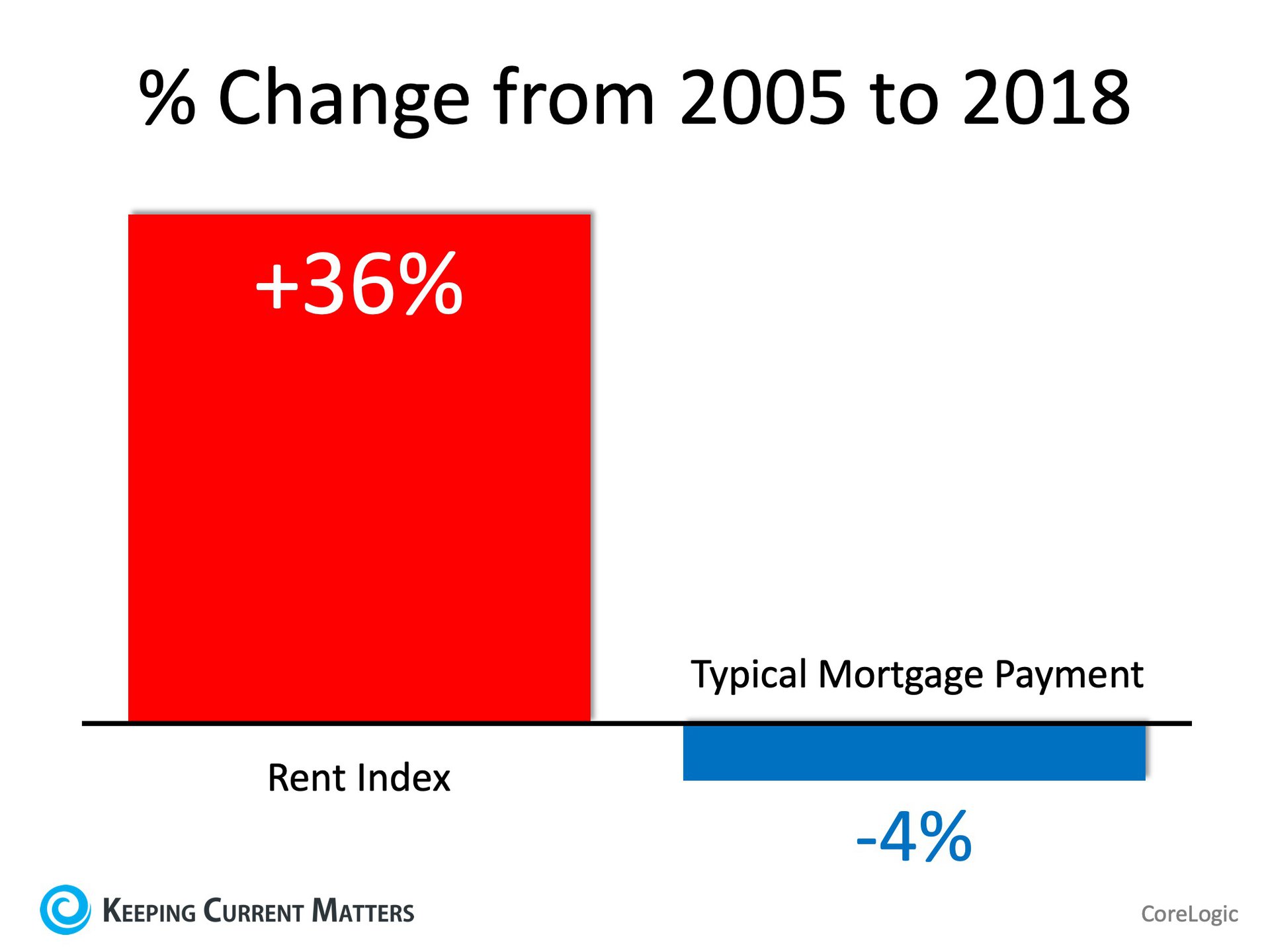

n a recent Insights Blog, CoreLogic reported that rent prices have skyrocketed since 2005. Meanwhile, the typical mortgage payment has actually decreased.

“CoreLogic’s national rent index was up 36% in December 2018 compared with December 2005, while the typical mortgage payment was down 4% over that period.”

It makes sense that rents have risen. However, how did mortgage payments decrease? CoreLogicexplained:

“It’s mainly because mortgage rates back in December 2005 were significantly higher, averaging 6.3% for a fixed-rate 30-year loan, compared with 4.6% in December 2018.

The national median sale price in December 2005 – $190,000 – was lower than the $220,305 median in December 2018, but because of higher mortgage rates in 2005 the typical monthly mortgage payment was slightly higher back then – $941 – compared with $904 in December 2018.”

Additionally, a recent report by the National Association of Realtors (NAR) showed that purchasing a home requires less of your monthly paycheck.

According to the Economists’ Outlook Blog, NAR’s February 2019 Housing Affordability Index showed that the “percentage of income needed” to pay the typical mortgage has decreased the last three months.

What does this all mean to the current housing market? We think First American said it best in a post last week:

“The mortgage rate-driven affordability surge has arrived just in time… Rising affordability has already benefited home buyers and, if the lower rate environment persists, we’re in for a great spring home-buying season.”

Source: (www.keepingcurrentmatters)

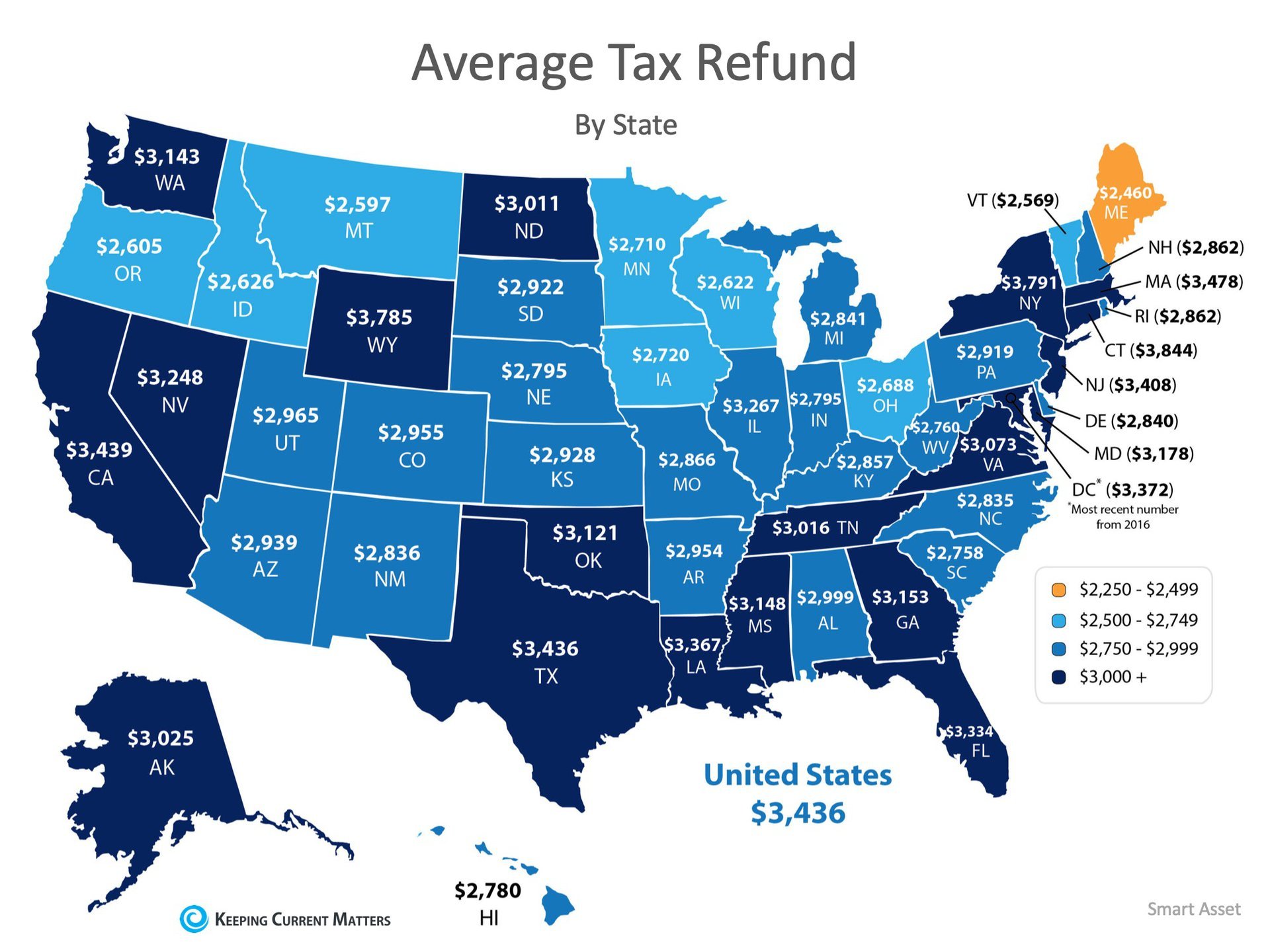

According to data released by the Internal Revenue Service (IRS), Americans can expect an estimated average refund of $3,143 this year when filing their taxes. This is down slightly from the average refund of $3,436 last year.

Tax refunds are often thought of as ‘extra money’ that can be used toward larger goals. For anyone looking to buy a home in 2019, this can be a great jump start toward a down payment!

The map below shows the average tax refund Americans received last year by state. Many first-time buyers believe that a 20% down payment is required to qualify for a mortgage. Programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae all allow for down payments as low as 3%. Veterans Affairs Loans allow many veterans to purchase a home with 0% down.

Many first-time buyers believe that a 20% down payment is required to qualify for a mortgage. Programs from the Federal Housing Authority, Freddie Mac, and Fannie Mae all allow for down payments as low as 3%. Veterans Affairs Loans allow many veterans to purchase a home with 0% down.

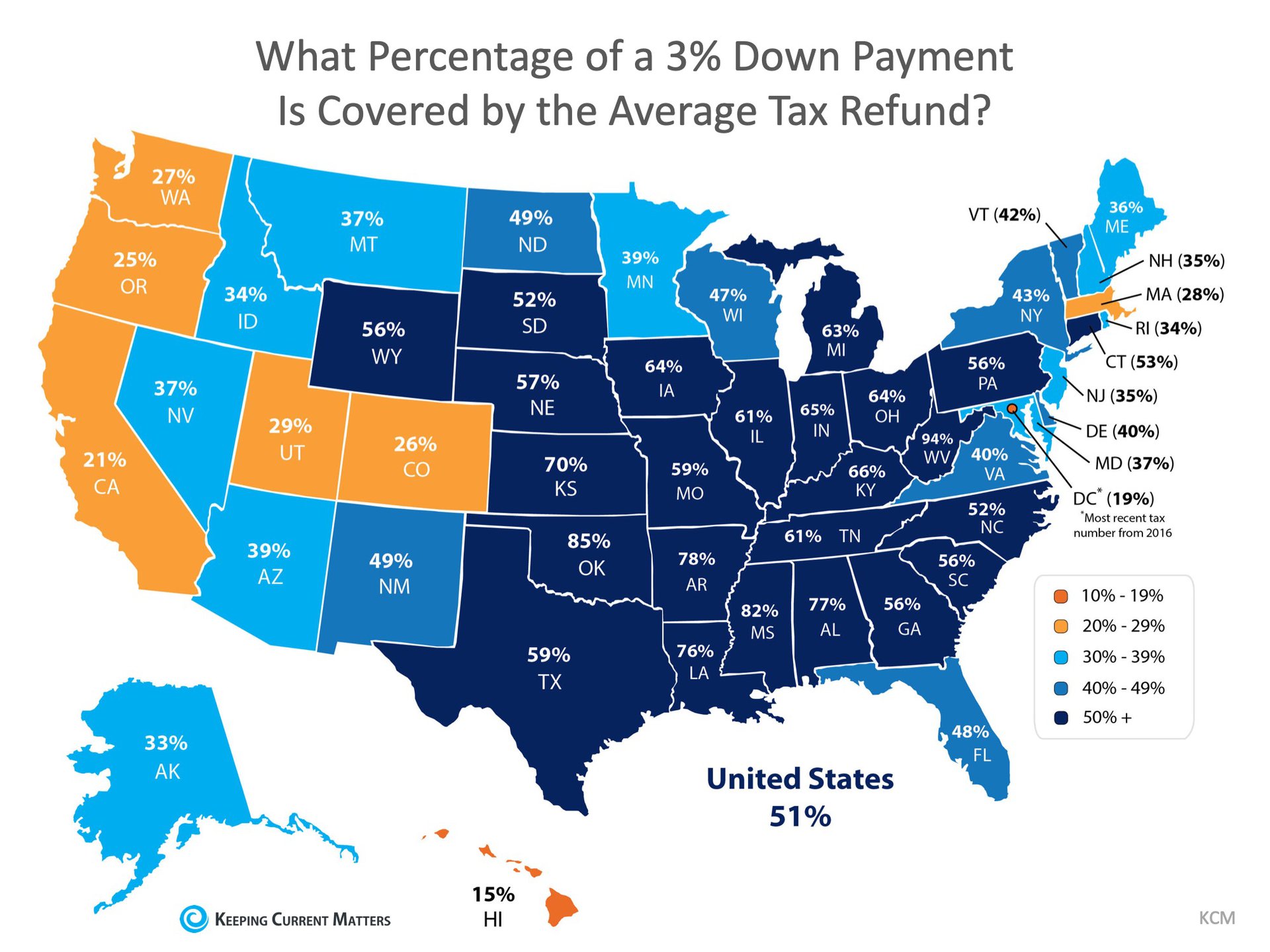

The map below shows what percentage of a 3% down payment is covered by the average tax refund by taking into account the median price of homes sold by state. The darker the blue, the closer your tax refund gets you to homeownership! For those in Oklahoma looking to purchase their first homes, their tax refund could potentially get them 85% closer to that dream!

The darker the blue, the closer your tax refund gets you to homeownership! For those in Oklahoma looking to purchase their first homes, their tax refund could potentially get them 85% closer to that dream!

Saving for a down payment can seem like a daunting task. But the more you know about what’s required, the more prepared you can be to make the best decision for you and your family! This tax season, your refund could be your key to homeownership!

Source: www.keepingcurrentmatters.com

Just like our clocks this weekend, in the majority of the country, the housing market will soon “spring forward!” Similar to tension in a spring, the lack of inventory available for sale has been holding back the market.

Many potential sellers believe that waiting until Spring is in their best interest. Traditionally, they would have been right.

Buyer demand has seasonality to it. Usually, this falls off in the winter months, especially in areas of the country impacted by arctic conditions.

Demand for housing has remained strong as mortgage rates have remained near historic lows. Even with an increase in rates forecasted for 2019, buyers are still able to lock in an affordable monthly payment. Buyers are increasingly jumping off the fence and into the market to secure a lower rate.

The National Association of Realtors (NAR) recently reported that in 2018 the top 10 dates sellers listed their homes all fell in April, May, or June.

Those who act quickly and list now, before a flood of increased competition, will benefit from additional exposure to buyers.

If you are planning on selling your home in 2019, meet with a local real estate professional to evaluate the opportunities in your market.

Source: (www.keepingcurrentmatters.com)

Source : (www.keepingcurrentmatters.com)

SOURCE: (www.keepingcurrentmatters.com)

One of the most common loans you can get to buy a home is a 30-year fixed rate mortgage. If the thought of paying for your home over the course of 30-years seems daunting, here are some easy ways to shorten that term which will actually end up saving you money over the life of your loan.

Any additional payments to the principal amount (the original sum of money borrowed in a loan), helps to cut down the amount of interest that you will pay over the life of your loan and can also help to shave years off the loan as well.

When you make ‘extra’ payments toward your loan, the key is to let your lender/bank know that you want the extra funds to go toward your principal balance as they will not automatically do this for you.

You don’t have to double your mortgage payment to make a big difference either!

If you have a 30-year mortgage on a median-priced home ($250,000) with a 5% interest rate, you’ll be responsible for a $1,342.05 monthly principal and interest payment. Over the course of the loan, if you pay your exact monthly payment, you will have paid $233,133.89 in interest alone!

Benefit: In the example above, adding $111.84 to your monthly mortgage payment might not seem like a lot, but each year you will have paid one extra month’s worth of payments which will shorten the term of your loan by 4 years and 8 months, all while saving you $42,000 in interest!

Benefit: Fifty dollars might not seem like enough to make a difference on the term of your loan, but that small amount will save you over $21,000 in interest and will take over 2 years off the end of your loan. Twenty-eight years from now, you’ll be happy to pay off your loan that much sooner!

Benefit: If you find yourself with a little extra money after a yearly bonus, a tax return, or from investment dividends, paying that money towards the principal can cut your costs. This option, however, is less predictable than the extra monthly payments.

If you have higher interest debts, like credit cards, consider using any extra funds you have to pay those debts down before applying that money towards your mortgage. Also, if you do not plan on staying in your home for more than 10 years, paying extra toward your mortgage might not make sense.

If you’re wondering what strategies would work best for you to shorten the term of your loan, consult a local real estate professional who can answer your questions or connect you with someone who can.

Source: (www.keepingcurrentmatters.com)